Sales charts based on public data are helpful, but they aren’t the full market.

One reported sale provides investors with one dot on a chart they can see. It might display the domain, price, extension, marketplace, and date of sale. Sometimes the buyer is disclosed. Sometimes the seller includes commentary on how they acquired the name years prior.

Brokerage sales can remain undisclosed.

Buyers can ask brokers to keep their identity confidential before negotiating. Sellers can agree not to discuss pricing. Brokers can confirm a sale was made without revealing price. Or, a domain may quietly transfer to a new company website without acknowledgement for months.

This poses a practical valuation challenge. Public historical sales data reflects only confirmed transactions in the public eye. It doesn’t map private sales.

Defining Non Disclosed Domain Sales

Transactions are considered non disclosed when certain details (price, buyer, seller, terms) are not publicly disclosed.

Oftentimes it’s for a legitimate business reason, not a nefarious one.

Companies may be planning a product launch and don’t want competitors to know. Founders might not want to spur expectations. Buyers may not want future sellers to assume they have a large budget for every variant. Sellers simply may want privacy.

And privacy is possible since the aftermarket has no central public repository. There’s no set-place where every domain transaction is publicly taped.

NameBio maintains an extensive database of public domain sales totaling over $3 billion. Reported is the key word here. NameBio is wonderful for researching comparables but does not pretend to list every transaction ever agreed upon.

Estimating Undisclosed Domain Sales Volume

It wouldn’t be useful to give a universal estimated percentage of non disclosed sales.

Brokers vary on how many sales they keep confidential. Marketplaces publish select results. Some sellers will voluntarily disclose their purchases. Other sellers say nothing.

Confidentiality also varies by market segment being analyzed.

Lower valued marketplace sales are easier to observe. Higher valued category domains tend to involve more privacy. Corporate upscales and privately brokered purchases are more secretive. A company writing a big check for a strategic domain may have little incentive to announce the dollar amount.

Instead, simply describe what you know about the visible dataset.

Public sales charts contain disclosed transactions. Public sales are what we know about. Not every sale that exists.

Calculating The “Shadow” Market Multiple

If you want to estimate the size of the undisclosed market you can’t state it as fact. You can create scenarios.

Start with an internal Excel model with the publically reported transaction value:

Assumed Non Disclosed Market Multiple x Publicly Reported Sales Value = Estimated Total Sales Market Scenario

Consider how sensitive the estimate is by changing the multiple. An assessment would be better served by publishing the assumed multiple it used, explaining its rationale, and framing the result as a modeled domain market capitalization vs. an audited one.

Why Some Big Sales Remain Private

Privacy can protect negotiating advantage.

A company may purchase a short brand domain for millions of dollars. Revealing the cost publicly could allow other sellers to inflate their price expectations for similar names they control. Competitors could also speculate that a new product is coming.

Privacy can limit distractions as well.

A buyer may want customers to care about the product, not how much they paid for the domain name. Sellers may not want to be approached by journalists, investors, or other speculators about their payout.

Sometimes confidentiality is tossed aside.

The Financial Times reported that AI. com was sold for $70 million dollars by Kris Marszalek, co-founder and CEO of Crypto.com. The article went on to highlight that this was the largest domain sale publicly announced at the time.

This was a public announcement because the details became public. Larger transactions sometimes don’t.

Non Disclosure Agreements & Domain Values

Undisclosed sales limit the public number of comps available to valuators.

Researching the value of a premium one word .com could uncover dozens of public sales. But private transactions are still missed. The public median provides helpful data, but is incomplete.

Which creates an edge for informed domain brokers.

An insider may know current market demand from private discussions, offers they can’t name, and past sales they can’t disclose. Someone looking at the public sales chart is missing pieces of the puzzle.

Instead of guessing, expand the range of disclosed public sales.

Add ranges to

scarcity, buyer fit, extension popularity, traffic, legal risks, strategic

value. Then record that it’s an estimate.

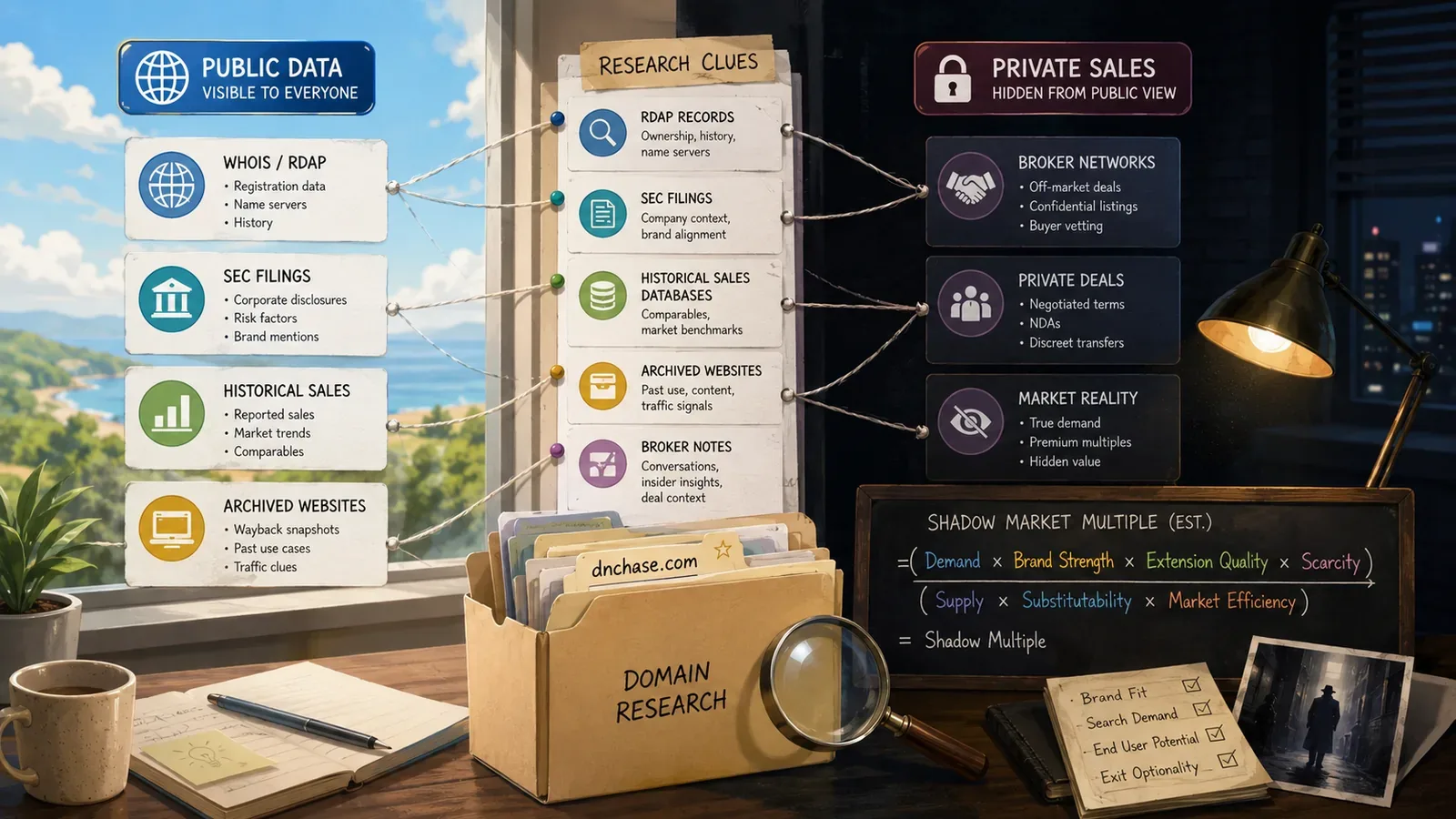

Calculating Sales From Public Information

While a private sale price can’t always be discovered, there can be clues left on public record.

On January 28, 20 25 ICANN announced that RDAP had been adopted as the standard for generic top level domain lookup. Registered Domain Access Protocol can surface the registrar, status codes, nameservers, and some changes even when personal data is removed.

Domain researchers can also research companies at the SEC EDGAR search page. The US Securities and Exchange Commission describes its search as covering 20+ years of filings. Results can be filtered by organization, filing type, keyword, and date.

The sales price of a domain may still be private.

Public companies may include acquisitions, goodwill, or intangible assets in a financial note without specifying a single domain name. Related filings can help form an opinion, but won’t always directly state a price.

Researching Off Market Sales – A Safe Protocol

A protocol is a predefined set of steps used to perform a task. Here’s a safe one to follow when looking into historic off market premium domain sales:

|

Step |

Action |

|

1. |

NameBio search for any public sales comps. |

|

2. |

RDAP lookup to document registrar, nameserver, and status updates. |

|

3. |

Document the live site and archive.org history. |

|

4. |

Check SEC EDGAR if the suspected purchaser is a public company. |

|

5. |

Review any press releases, executive tweets, trademark applications, or legitimate news coverage that surfaces. |

|

6. |

Mark your findings as confirmed, inferred, or unknown. |

|

7. |

Don’t publish leaked info or NDA protected details. |

Buyers can also request that a broker keep their identity confidential. According to GoDaddy, Domain Broker Service purchases from their escrow keep the buyer anonymous throughout negotiations.

Conclusion

Public information is valuable because it’s public.

Non disclosed domain sales don’t render public sales charts meaningless. Non disclosure simply requires you to use the data wisely.

Let public sales give you a baseline. Use public records to uncover technical and corporate hints. Apply a multiple to create a range. Publish unknowns as unknowns.